STOP ROBBING PETER TO PAY PAUL. THERE IS A WAY OUT.

Finally - A Clear, Step-By-Step System For People With £6,000+ Across Multiple Creditors: How To Stop The Debt Spiral, Slash What You're Paying Each Month, And Know Exactly What To Do Next

(even if you've already tried consolidation loans, budgeting apps, and "just calling your creditors" - and nothing's worked)

The System That's Transforming "I Don't Know How I'm Going to Make It to Payday" Into "I Have a Plan - And It's Actually Working" - In As Little As 30 Days

"I feel like I'm constantly reshuffling debt around. Pay one off with a loan, then spend the loan money to survive, then back to the cards. It's just been an endless cycle of trying to stay afloat... I'm basically one month away from everything collapsing."

Does that sound familiar?

You're not a reckless person.

You're not stupid with money.

But somewhere along the way - maybe a job loss, a relationship breakdown, a period of just trying to survive - the debts stacked up.

And now you're sitting here with multiple creditors all wanting their cut of a salary that just.

Doesn't.

Stretch.

Far.

Enough.

You open your banking app and immediately close it again.

You feel your stomach drop when a number you don't recognise calls.

You've been paying the minimums on four different things, moving money around between accounts like a shell game, telling yourself "next month I'll get on top of it"

And next month comes and goes and the numbers are somehow worse.

You've stopped talking about it.

You've told yourself it's fine.

You've googled solutions at midnight and closed seventeen browser tabs without doing anything, because the information is so confusing, the options are so overwhelming, and frankly - it's easier to just not think about it for one more day.

Now, the thing keeping you up at night looks something like this:

You're juggling multiple creditors - loans, credit cards, overdrafts, store cards - and you genuinely can't remember what you owe to who anymore

The minimum payments alone are crippling - you're left with nothing after payday, or you're using credit to cover everyday essentials like food and petrol

You've heard of debt management plans, IVAs, bankruptcy - but you have absolutely no idea which applies to you, or whether any of them will make things worse

You're terrified about your credit file - that it's already wrecked, or that getting help will wreck it more

You're hiding the situation from someone - a partner, your family - and carrying the weight of it completely alone

And the worst part?

You feel like this is your fault.

Like you should have known better.

Like everyone else is managing fine and you're the only person drowning.

You are not the only person drowning.

Millions of people in the UK right now have more than £6,000 across multiple creditors and no clear plan for getting out.

The shame makes them suffer in silence.

The jargon makes them feel stupid.

The options feel overwhelming.

And every day they do nothing, interest compounds and the hole gets deeper.

I know because I've been there.

And I know because of what happens when you finally get clear on exactly what to do.

I Tried Everything Before I Found What Actually Works

I tried making a budget spreadsheet (every single time - it lasted two weeks before something unexpected blew it apart).

I tried the minimum payment strategy (just paid interest for two years and the balances barely moved).

I tried calling my creditors to explain (got passed around three departments, put on hold for 45 minutes, and given conflicting information that made me more confused).

I tried a consolidation loan (rejected - my credit score was already hammered from the missed payments and multiple applications).

I tried just "cutting back on everything" (you can't cut your way out when your minimum payments are already higher than what's left after your essential bills).

I tried googling "what to do about debt UK" (got 47 different websites, contradictory advice, and absolutely no idea what my actual options were in my actual situation).

And here's what I learned when I finally found my way through...

According to research from the Money and Pensions Service, over 9 million people in the UK are in serious financial difficulty - yet fewer than 20% ever seek advice. Not because help isn't available, but because:

People don't know where to start

They don't understand their legal rights as debtors

They're terrified that getting help will make things worse

The information available online is either too complex or tries to sell them something unsuitable

The shame and secrecy stops them asking anyone

The key insights that changed everything for me:

There are formal, legal protections available in the UK that most people in debt have never heard of - including the ability to freeze interest and pause creditor contact while you get sorted

The "obvious" solutions (consolidation loans, balance transfers) are often the worst move for people with multiple debts above £6k

Creditors are almost always willing to negotiate - they have legal obligations about how they treat customers in financial difficulty, and you have rights most people never use

Your credit file situation is almost certainly better than you think, and every option available to you has a path to recovery

The difference between people who drown in debt for a decade and people who get out in 3-5 years is not income. It's having a clear, informed, sequenced plan.

But most importantly of all:

Most people in debt are making the exact same mistakes - mistakes that cost them thousands of pounds and years of their lives - not because they're bad with money, but because nobody ever gave them a clear system.

I know, because I was making all the same mistakes...

Through extensive research, personal experience, and working with:

Debt advice specialists and FCA-regulated advisers

People who've successfully navigated IVAs, DMPs, and DROs

Real accounts from hundreds of people who shared their situations on UK debt forums

I discovered exactly WHY the standard advice fails - and, more importantly, what actually works when you have £6,000+ across multiple creditors in the UK.

I Call It 'The Debt Exit Plan'

By giving you a complete, step-by-step framework for understanding your situation, choosing the right solution, and executing your plan, The Debt Exit Plan will help you:

Finally know exactly what solution is right for YOUR situation - not a generic internet answer, but a framework you can apply to your specific debts, income, and circumstances

Reduce your total monthly outgoings - often dramatically, without it being your "fault" or damaging your life more than necessary

Stop the creditor calls, letters, and anxiety - using your legal rights that most people in debt never even knew they had

Protect what matters most - your home, your car, your job, your relationships - while you deal with this properly

Understand your credit file - what it actually says, how long the impact lasts, and exactly how you rebuild it after

Get free - with a realistic, personalised timetable so you can see the end of the tunnel for the first time

THE DIFFERENCE BETWEEN PEOPLE WHO SPIRAL FOR YEARS AND PEOPLE WHO GET OUT

The 5 Essential Skills People With £6,000+ Across Multiple Creditors Need (That Google, Generic Budget Advice, and Well-Meaning Friends Don't Provide)

1. Knowing Your Priority Debts From Your Non-Priority Debts: Understanding which debts can lead to losing your home, your freedom, or your essentials - and which (despite feeling urgent) are actually less dangerous. Most people focus their money and stress completely backwards. If you get this wrong, you can fix a smaller problem while losing something you can't replace.

2. Understanding the UK Debt Solution Landscape:

There are at least 8 different formal debt solutions available to people in the UK, each with completely different eligibility criteria, costs, and consequences. Choosing the wrong one doesn't just waste time - it can lock you into something inappropriate for years, or cost you tens of thousands of pounds in unnecessary fees.

3. Knowing Your Legal Rights as a UK Debtor:

You have rights most people in debt have no idea about. Creditors must follow strict FCA rules. You can access Breathing Space. You can challenge affordability. You can make legitimate complaints. Not knowing this means creditors can bully and pressure you into agreements that don't serve you - and often, that's exactly what happens.

4. The Budget Reset Method:

Not a budget in the usual sense. A structured, priority-based allocation system that starts with what you must keep, works through what you should pay, and finally addresses what creditors are demanding you pay - in that order. This changes everything about how you manage the next 12–36 months.

5. The Rebuilding Phase Roadmap: Every debt solution has a defined recovery period. Most people know what happens during the hard part - but have no plan for what happens after. Without this, people exit debt solutions and slip straight back into the same patterns within 2 years. The exit is only the beginning.

GET INSTANT ACCESS — START TAKING BACK CONTROL TODAY

Here's Everything You Get With The Debt Exit Plan Today

What's included:

The Complete Debt Exit Plan: 7 comprehensive modules covering every stage of the journey from "I don't know where to start" to "I have a clear plan and I'm executing it"

🎁 Plus These 5 Targeted Bonus Guides 🎁

BONUS 1: "The Breathing Space Blueprint": How to Legally Pause Creditor Action For 60 Days While You Put Your Plan Together (£9 Value)

Most people in debt have never heard of the Breathing Space scheme - a legal protection introduced in 2021 that lets you pause almost all creditor action, interest, fees, and enforcement for 60 days. This short guide walks you through exactly who qualifies, how to apply in under 30 minutes, and how to use those 60 days strategically to set up the right long-term solution.

BONUS 2: "The Creditor Communication Scripts": Word-For-Word Templates for Every Situation (£9 Value)

One of the most paralysing parts of being in debt is not knowing what to say when creditors call or write. This bonus gives you tested, compliant scripts for: requesting a payment freeze, disputing a debt you believe was irresponsibly issued, responding to a debt collection company, requesting a Statement of Account, and making a hardship arrangement - so you never have to improvise a stressful conversation again.

BONUS 3: "The Credit File Recovery Timeline": A Month-by-Month Guide to Rebuilding Your Credit Score After Debt" (£9 Value)

Most people assume their credit file is ruined forever. It isn't - but rebuilding it requires doing specific things in a specific order. This guide gives you the exact 24-month timeline: what appears on your file and when it drops off, when to apply for a credit-builder card, what "good" looks like at 6, 12, and 24 months, and how to monitor your progress without it costing you more marks.

BONUS 4: "The Mis-Sold Loan Checklist": How to Know If You Were Irresponsibly Lent To (And What To Do About It)" (£9 Value)

Tens of thousands of UK borrowers are owed money back from lenders who issued loans without properly checking affordability. If you were approved for credit when your debt-to-income ratio was already high, this checklist walks you through the exact grounds for a complaint, how to file with the Financial Ombudsman Service, and what a successful claim looks like - with real examples. This bonus alone has helped people get thousands of pounds written off.

BONUS 5: "The Partner and Family Conversation Guide": How to Have the Conversation You've Been Dreading" (£9 Value)

Whether it's telling a partner you've been keeping this from them, explaining the situation to family members who might be affected, or asking for support you desperately need - this guide gives you a compassionate, practical framework for having the conversation. You'll know what to say, what to expect, and how to make the conversation a turning point rather than a crisis. Because carrying this alone is making everything worse, and you don't have to.

Normally: £92

Today: £4.99

BEFORE AND AFTER

The Transformation You Can Expect

Don't let debt continue dominating every area of your life. Your financial future can be calmer, clearer, and more manageable than it feels right now - you just need the right system to make it happen.

Before The Debt Exit Plan:

Waking up at 3 am running through the numbers again, trying to work out how to make this month work

Dreading payday - because you know the money will be gone before you can breathe

Ignoring calls from numbers you don't recognise and living in fear of what the next letter will say

Feeling like you're the only one in this situation - too ashamed to ask anyone for help

Googling the same things over and over and getting more confused with every answer

Taking on more debt to manage existing debt - a consolidation loan, a balance transfer, a PayPal Credit advance - and knowing deep down you're just delaying the inevitable

After The Debt Exit Plan:

A clear, written plan that tells you exactly what to do this week, this month, and for the next 12–36 months

A monthly payment that's actually affordable - often significantly less than you're currently paying

Creditors handled - through the proper channels, using your legal rights, so they're no longer calling and you're no longer hiding

Understanding of exactly how long your situation will take to resolve - and what life looks like when it does

Your credit file explained and a realistic recovery path mapped out

The secret lifted - a script for telling the people in your life, and a way to move forward together

YOUR PATH TO DEBT FREEDOM STARTS HERE

The 7 Modules That Take You From Overwhelmed and Stuck To Clear, Calm, and In Control

Each module is designed to build on the last - so by the end, you don't just understand your situation, you have your complete personalised action plan.

MODULE 1: The Full Picture - How to Get Total Clarity on What You Actually Owe (And to Whom)

(Complete in 1–2 hours)

This module breaks through the fog. We start by getting every single debt - known and half-forgotten - out of your head and onto paper. You'll learn how to pull your credit report for free, understand what every entry means, identify any errors that could be costing you, and create your master debt list. By the end of Module 1, you'll know exactly where you stand - probably for the first time in years.

The free credit report method that shows you every creditor who has a record of your debt

How to identify "phantom debts" that may not even be legally enforceable

The priority vs non-priority framework that tells you which debts matter most right now

A fillable Master Debt Tracker template so everything is in one place

MODULE 2: Your Budget Reset - What You Actually Have Available (And Why That Number Changes Everything)

(Complete in 2–3 hours)

Most debt advice starts with "you need to budget better." This module takes a completely different approach. We're not cutting your Netflix to pay a credit card. We're building a legally-informed, priority-first financial picture that gives you the number that every debt solution in the UK is based on: your available income. This is the number that determines which solutions you're eligible for - and how affordable your plan will be.

The UK-standard income and expenditure format used by every creditor and debt adviser in the country

What counts as an "essential" expense - and how to make sure you're not leaving money on the table

Common mistakes that make people's available income look higher than it actually is - and what creditors try to exploit

Your Available Income Calculator - the single number that drives your next steps

MODULE 3: Mapping the Landscape - Every UK Debt Solution Explained in Plain English

(Read time: 60–90 minutes)

This is the module most people wish they'd had years earlier. It covers every formal debt solution available in England, Wales, and Scotland - DMP, IVA, DRO, Bankruptcy, Administration Order, Breathing Space, and Consolidation - with honest explanations of who each is for, what the real costs and consequences are, how long they last, and what the impact on your credit file looks like. You'll finish this module knowing more about UK debt solutions than most people who've been struggling for years.

Debt Management Plan: when it's the right call and when it drags out unnecessarily

Individual Voluntary Arrangement: the powerful tool that can write off significant debt - and the scams to avoid

Debt Relief Order: the underused solution for smaller debt balances that can wipe the slate completely

Bankruptcy: what it actually means, what it doesn't mean, and who it genuinely suits

The myths that keep people from choosing the right solution - debunked

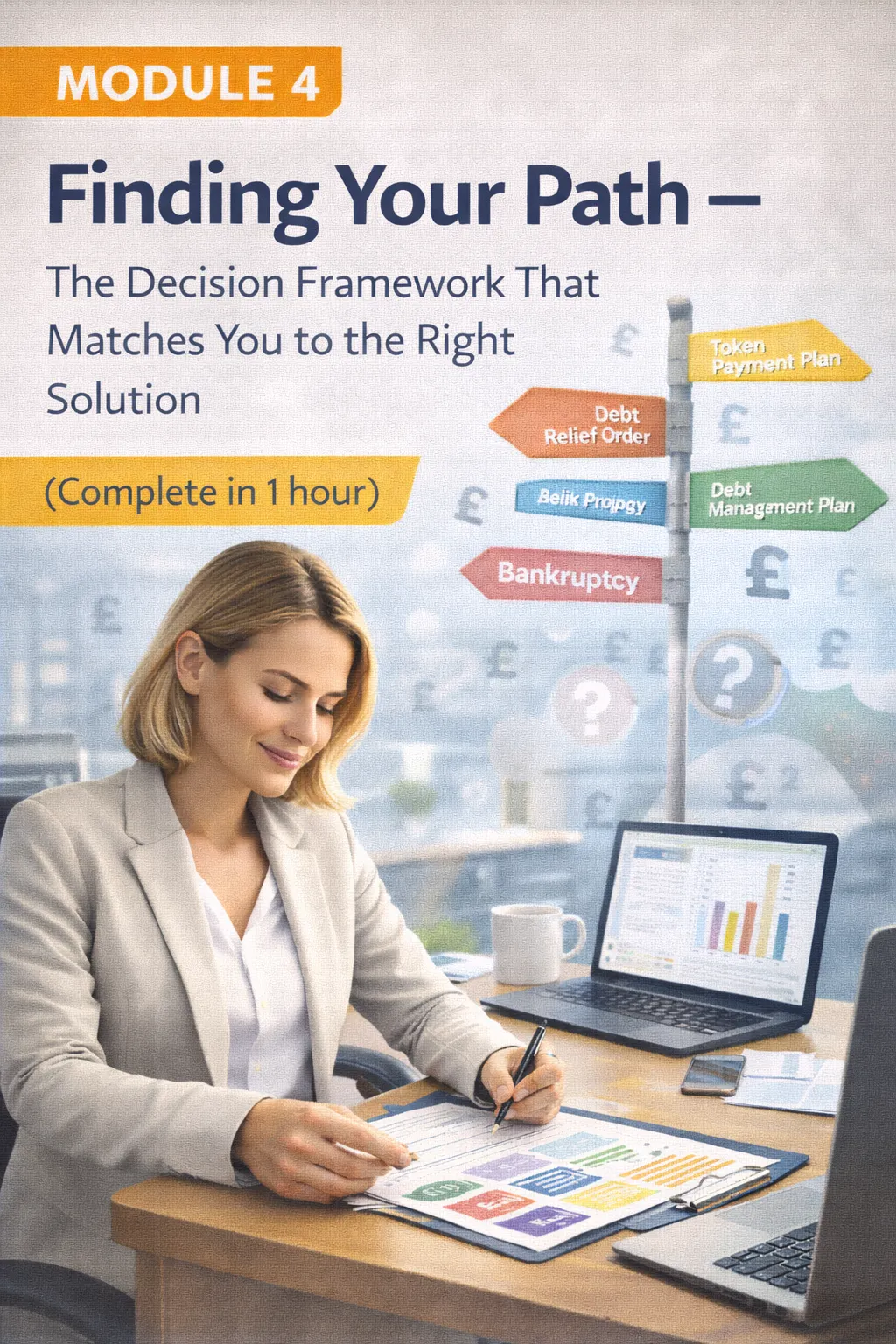

MODULE 4: Finding Your Path - The Decision Framework That Matches You to the Right Solution (Complete in 1 hour)

This is where you stop reading and start deciding. Module 4 gives you a step-by-step decision framework that - based on your specific debt total, creditor mix, income, circumstances, and priorities - points you toward the solution most likely to be right for you. You'll also learn how to verify this with a free, no-obligation conversation with a UK debt charity, so that your choice is informed and confirmed before you commit.

The Debt Exit Decision Tree - a clear, branching framework based on your real numbers

How to prepare for a free debt advice appointment so you get the most out of it (not every adviser is equal)

Red flags that indicate you're being steered toward an option that benefits the company, not you

How to access Breathing Space immediately if creditors are already taking action against you

MODULE 5: Executing Your Plan - The Step-by-Step Process for Whichever Route You Choose

(Reference module - revisit as needed)

This module walks you through the practical execution steps for each major solution, so nothing comes as a surprise. What happens when you contact StepChange? What does an IVA application actually involve? How does the DRO process work? What do you need to say to creditors who call while your plan is being set up? This module gives you the exact sequence so you can follow the process with confidence.

The three free debt charities you should always work with (and why to avoid commercial debt management companies)

Creditor communication protocol during the setup phase - what to say, what not to say

How to handle creditors who refuse to cooperate - your formal escalation rights

What the first 30, 60, and 90 days look like in practice for each solution

MODULE 6: Protecting What Matters - Your Home, Your Job, Your Essential Life

(Read time: 45–60 minutes)

One of the biggest fears people carry is that dealing with their debt will cost them something precious - their home, their employment, their security. Module 6 addresses this directly and honestly. You'll understand the real risks (and they're probably not what you're afraid of), what actually threatens your home versus what doesn't, how different debt solutions interact with tenancies and mortgages, and how to handle any employment-specific concerns.

Which debt solutions affect tenancies and mortgages - and which genuinely don't

The jobs and professional roles where certain debt solutions require disclosure - and how to get proper advice if this applies to you

How to protect a joint account or a financial relationship from the fallout of individual debt

What "bailiff visit" actually means legally - and the specific situations where it can and cannot happen

MODULE 7: Life After Debt - Your Credit Recovery and Rebuild Roadmap

(Complete in 30–45 minutes)

The single most underserved chapter in debt advice. This module gives you the complete post-solution roadmap: what your credit file looks like at every stage, the exact steps to begin rebuilding your credit score, how long before you can get a mortgage again, what healthy financial habits look like for someone who's been through this - and how to make sure you never end up back here. This chapter is about building a genuinely different relationship with money.

The 6-year credit file timeline - what appears, when it drops off, and how to track your progress

The Credit Builder Protocol - a step-by-step 24-month plan for rebuilding a healthy credit profile

The psychological patterns that lead back to debt - and how to interrupt them

Building your first proper emergency fund - even while you're on a repayment plan